Know your customer (KYC): Then, now and where to next

Table of Contents

Anyone who has engaged with financial institutions, currency exchanges or nimble fintech startups long enough has heard the term ‘know your customer’ (KYC). Compliance varies by country, but the gist of it is the set of regulatory requirements that financial enterprises must meet in order to verify new and current customers.

Initially a document-heavy process, today’s KYC is leaps and bounds ahead of the paper-laden protocol of even a decade ago, thanks to advances in AI.

While it is interesting to trace the roots of KYC, it is even more interesting to see where technology is taking this area of business. But first, we will touch on exactly what this entails.

What is KYC?

A rigorous data-driven process, KYC requirements include identity verification, such as liveness checks and governmental authentication, background checks, such as watchlist screening and adverse media reviews, and enhanced due diligence to gauge individual client risk profiles.

The bottom line: you need to ‘know your client’, at least from a risk perspective. It’s not just about ticking a legal box. It’s about countering the very real and increasing threat of fraud and money laundering.

Then there’s the PR nightmare that comes from unknowingly entering into business with shady and unscrupulous clients, or even sanctioned customers and downright criminals.

The Origins of KYC

So, where did it all begin?

As one of the first anti-money laundering (AML) regulations worldwide, the US Bank Secrecy Act of 1970 is worth mentioning, having paved the way for mandatory and precautionary record-keeping and reporting from financial institutions. Countries around the world slowly followed suit, with varying local regulatory nuances.

In South Africa, KYC was initiated following the Financial Intelligence Centre Act (FICA) of 2001, which established the Financial Intelligence Centre (FICA) and legislated AML and countering terrorist financing (CTF) protocol for accountable institutions.

Of course, this was initially a lengthy process, fraught with frustration on both the customer and company front, and one too many trips to the printer. KYC documents, such as proof of identification, address and source of funds, including payslips and bank statements, required in-person verification.

Without modern AI-driven AML solutions, the authenticity of a document had to be determined manually.

From an adverse media and watchlist screening perspective, sanctions and politically exposed person (PEP) screening was performed utilising curated lists obtained from data bureaus, where rescreening could take place as lists were updated on an ad hoc basis.

The Digital Transformation of KYC

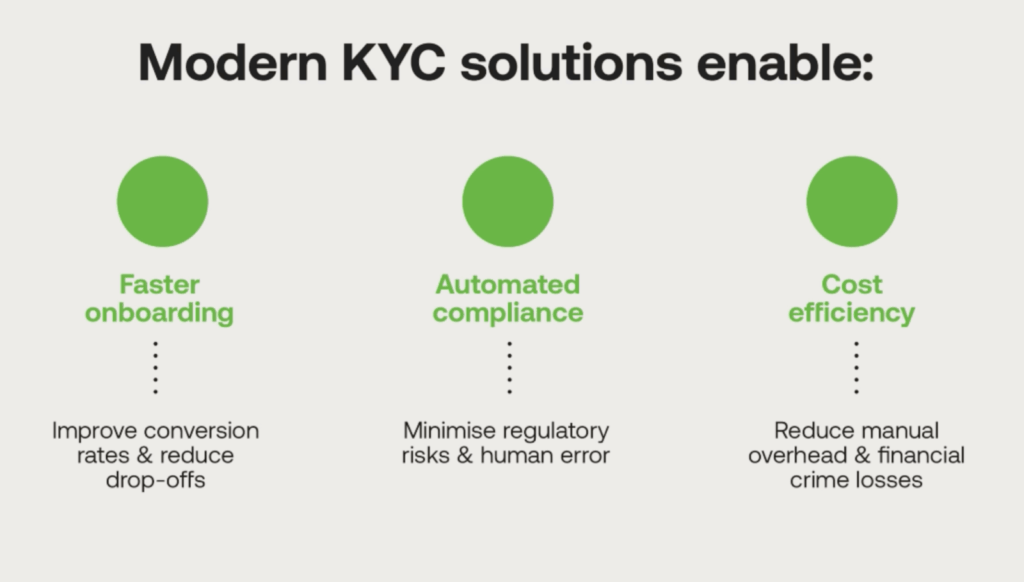

AI changed the game for KYC verification, where advances in machine learning and natural language processing brought about swifter, smarter customer onboarding.

Significant shifts took place with the help of AI and improved digitisation, such as the online verification of KYC documents, facial recognition through video and the acceptance of electronic signatures.

The Future is Perpetual Monitoring

AI will take the future of KYC further still, where continuous screening will become the norm.

Known as perpetual KYC, this digitally-driven process hooks into an array of data sets to ensure reliable and up-to-date customer information.

In contrast to ad hoc updates, it is about adjusting your client risk profile in near real-time, based on daily adverse media and watchlist screening measures.

Not only is risky and suspicious behaviour on the part of your client an issue to be flagged, but KYC tools of the future are emphasising relationship mapping. Should a family member or close tie of your customer become a sanctioned person, this raises the risk associated with that client and is something a company ought to know.

With modern technology, detecting fraud and money laundering is fast becoming a dynamic process, fully automated, accurate and engaged in real-time investigation.

KYC Beyond Financial Institutions

While KYC originated in banking, regulations extend across the financial sector. Insurers, lenders, fintech startups, cryptocurrency exchanges, auction houses, and even auto dealers must verify customer identities and screen for red flags.

Strict KYC protocols are central to a robust AML and CTF strategy for any business handling significant financial transactions.

No Compliance Shortcuts

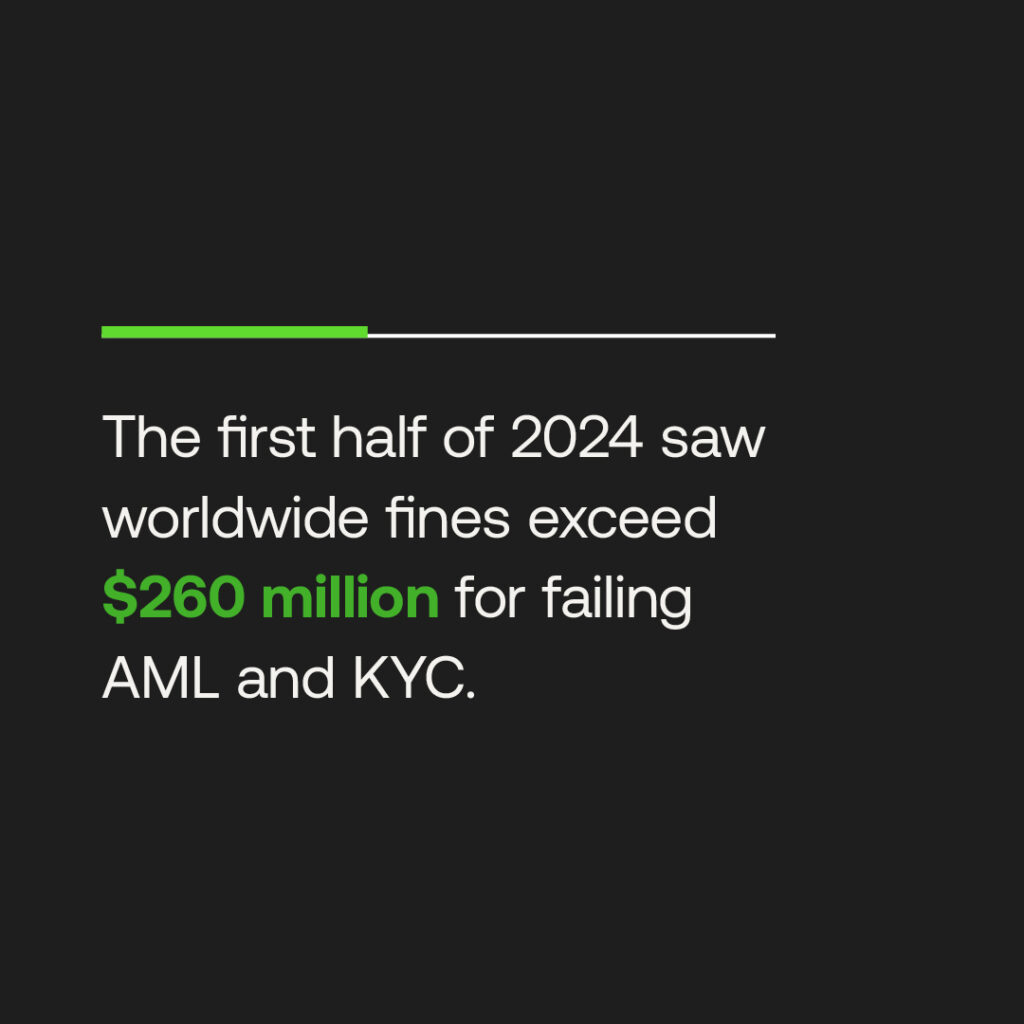

Fraud and money laundering present major risks across the financial landscape. Failing to establish strong KYC procedures can have severe consequences including hefty fines, criminal prosecution, and damage to an institution’s reputation.

Our cloud-based AI-powered end-to-end KYC and AML/CTF solution is a suite suited for compliance in the future.

As financial crime continues to surge globally and regulation tighten, it makes business sense to turn your compliance over to the experts.

Disclaimer

This article is intended for educational purposes and reflects information correct at the time of publishing, which is subject to change and cannot guarantee accurate, timely or reliable information for use in future cases.