The cost of AML CFT compliance

Table of Contents

How to balance efficiency and effectiveness

In the battle against financial crime, compliance officers may feel like middlemen, but understanding the cost of AML CFT compliance is crucial to properly budget and staff anti-money laundering and counter-terrorist financing programs, which have become far more strict in financial services.

Staying up-to-date with a complex, ever-changing fin crime landscape is a feat that has yet to be achieved. The consequences could be devastating without compliance officers in the hot seat to ensure effective customer and employee due diligence.

We’re not just talking about high fines for falling short of audits or irrefutable reputational damage, but also real-world impact from arms smuggling, human and animal trafficking, or the Proliferation of Weapons of Mass Destruction (CPF), lining the pockets of crime networks around the world.

It sounds impossible when businesses call on compliance professionals to fulfil mandatory AML/CFT obligations while keeping costs down. But striking the right balance is about working smarter, not harder: pre-planning to smooth processes and calling on cost-effective technology to help at every stage.

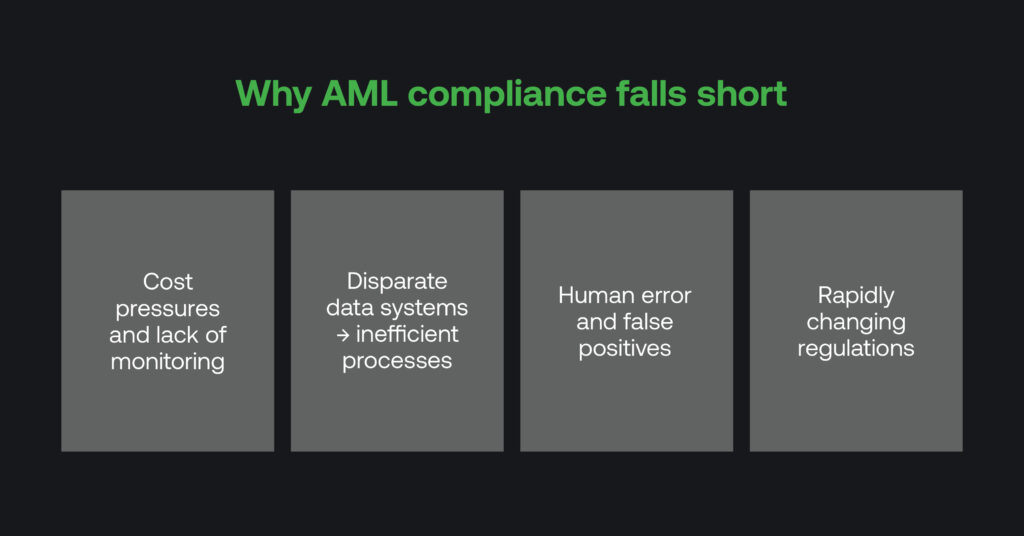

What causes AML compliance deficiencies?

“Cost pressure and balancing competitive and compliance pressures were reported as key challenges, yet 45% of respondents did not monitor their cost of compliance with regulations across their organisations.” Thomson Reuters 2023 Cost of Compliance Report

Compliance officers within financial services recognise the considerable ‘cost of compliance’ involved with onboarding and continuously monitoring transactional data. But there are gaps in what’s required to streamline every compliance stage and remain on board with regulators. The truth is that ineffective systems add up to significant sums, not just financially.

Analysts need more time to process vast amounts of data by hand, which is also highly susceptible to error. The human eye can miss valuable data or incorrectly flag legitimate information; these false positives kick off another endless cycle of unnecessary manual workload to correct mistakes.

With data spread across multiple systems, disparity hinders compliance efforts and puts a vast, money-draining strain on resources that are more valuable elsewhere. Instead, a single view of a customer’s information is necessary to determine and analyse risk.

Regenerating regulations: help or hindrance?

Not that condensing anything to a single point within AML compliance is easy. Compliance requires great agility; regulations change so fast that they force a massive weight on a compliance officer’s shoulders.

Following international standards agencies, including the Financial Action Task Force (FATF) and multiple local authoritative bodies, there is a requirement to adapt, absorb, and implement every legislative detail. Even after getting to grips with one round of regulation, another revision will duly rear its head…

But standards must change when more strands are added to a financial criminal’s web. While it may seem inconvenient, regulators act as the front line against terrorists, launderers, and traffickers, who could easily carry on undetected otherwise. In particular, FATF periodically revises its 11 key recommendations to improve firms’ effectiveness in their AML compliance. Likewise, businesses must hire compliance officers to stay abreast of new releases.

A company can only mitigate risk from unchecked due diligence and monitoring protocols by understanding the ins and outs of the compliance landscape. By combining a network of regulators, dedicated compliance professionals, and technology platforms, a more robust fight against criminals around the globe can be established.

Crafting a compliance-first culture

In this case, obligatory regulations do not hinder efficiency and can be viewed as blueprints for compliance officers to formalise an effective onboarding and screening system. Risk assessments lay the mandatory groundwork for any compliance strategy, where institutions can identify any flaws or overheads in their existing AML processes that fall short in identifying persons with criminal convictions and associations, politically imposed sanctions, or otherwise.

Risk assessments can take into account a range of internal factors. Smaller firms may have tighter budgets, customer bases, and services, or operate in areas less susceptible to financial crime. Larger financial institutions, on the other hand, may work across borders and deal with high net-worth clients and need to create a standardised, holistic risk assessment framework from the top down, which can be periodically reviewed.

After determining their best quality control route, compliance officers can structure effective internal policies and procedures companywide and help employees understand crucial AML regulatory requirements and any repercussions for malpractice. Building this compliance-first culture enables every business area to place reputational risk at the forefront of their minds and organise themselves for any external audit.

Technology, the complementary compliance partner

With firm parameters set out in a risk assessment, investing in technology can cut the laborious and costly heft of AML/CFT compliance processes by automating every long-winded manual task.

In particular, artificial intelligence (AI) tools can comb through and segment vast amounts of data in seconds to understand patterns, spot anomalous data or transactions, and alert compliance officers in real-time. It helps improve the data quality of investigations, lowers the number of false positives, and uses intelligent data matching to reduce unnecessary noise.

Technology solutions can also integrate with any pre-existing processes and risk-assessment frameworks and flexibly adapt to any changes in regulation with speed. Businesses become compliance-ready instantly, able to pinpoint investigative data to auditors within minutes; before, this could have taken human analysts weeks to complete.

Technology is not taking over the role of those at the regulatory helm. Compliance officers steer the whole machine, but when repeatable background tasks are automated, they can focus on maintaining risk oversight for the business and appeasing regulators. Ultimately, by saving time and money within AML/CFT processes, compliance professionals can better contribute to saving parts of the larger financial crime picture, too.

RelyComply’s AI-driven solution aims to boost efficiency with an end-to-end platform that can fit into your AML/CFT processes.

Disclaimer

This article is intended for educational purposes and reflects information correct at the time of publishing, which is subject to change and cannot guarantee accurate, timely or reliable information for use in future cases.