Why transaction integrity is the latest operational opportunity for AML compliance

For some time, firms stuck rigidly to rules-based AML transaction monitoring. But as time ticks on and the pace of digitalisation becomes extortionate, that mindset has dated itself very quickly indeed. Laundering activity can slip past the financial system when institutions do not implement real-time risk management. And the payments being pushed around the world are only as clean as the data-rich gatekeepers that facilitate their movements.

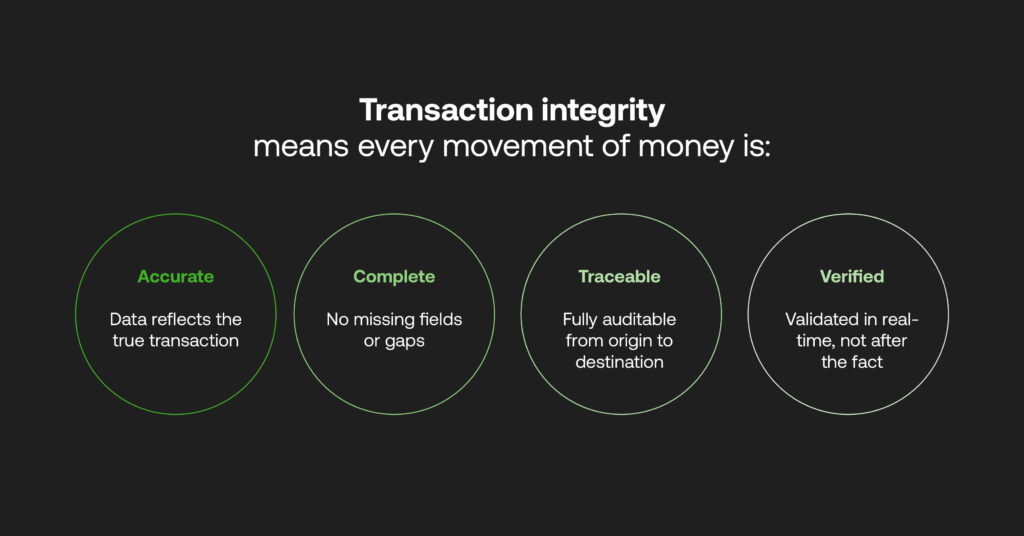

This is why ‘transaction integrity’ is now a regulatory expectation. What this means is that all recorded customer and transactional data a firm holds and tracks (including transfers, deposits, and withdrawals) must be fully validated as being truthful and compliant. Those that fail to demonstrate authenticated transactions will be under the spotlight, as a lack of integrity will lead to fragmented and delayed Suspicious Activity Reports (SARs) – as well as slowed payments that do not adhere to growing reconciliation regulations in the UK.

Already, banks working in or with the Eurozone must ensure payees receive funds instantly (and confirmation sent to the payer’s payment service provider, PSP) under the EU’s SEPA Instant Credit Transfer scheme, and fast payment systems are becoming a ‘new normal’ worldwide. Traceability throughout end-to-end compliance operations are pivotal to achieve this and reduce reputational risk; AML transaction monitoring is just one step of an overarching transaction integrity to stand institutions on the front-foot of compliance.

Table of Contents

Where firms’ audit trails fail

Despite transaction monitoring software being the skeleton of a modern AML compliance system – where the scanning and detecting of suspicious behaviour occurs – it does not account for full transaction integrity now championed by the UK’s regulators. Achieving operational assurance means that the whole payment facilitation process has to occur using verifiable data, with complete, accurate and instant alerts generated by monitoring models.

This is where many financial businesses’ preconceptions to traditional monitoring are tunnel-visioned. It’s only an assumption that, in these cases, transaction-level data is clean and auditable. The reality is that manual oversight for audit trails leads to significant vulnerabilities. Any lacking details creates unsubstantial SARs to be submitted to the National Crime Agency (NCA), and further disruptions to investigations that can affect a firm’s credibility.

Elsewhere under the FCA’s CASS enforcement (for the investor sector, but branching out to banks, payment and e-money institutions, and credit unions), firms must safeguard client or policyholder assets if the business fails – and return funds to them as soon as possible. As noted by the Bank of England, these shortfalls are exacerbated by poor operational frameworks. When funds are segregated poorly, it’s extremely difficult for firms to get visibility into rich customer data for reconciliation purposes, which can be daily or weekly.

Additional regulatory chokeholds

Transaction integrity has now recently grown to a severe regulatory expectation, as incomplete or siloed data can spell danger through aggregation risk. This applies to combining individual risks into a singular unit to decide a firm or entity’s total risk exposure. The method can miss the entire scope of wrongdoing, such as a beneficial owner masking their complete nefarious activity among multiple accounts and jurisdictions, or smurfed funds being treated as minor deposits rather than a network. Funds for genuine reconciliation can get lost in this maze when not segregated and protected.

The sheer volume of daily payments data available, and the diverse world of payment rails magnifies the risk of human error in manual reconciliations. The UK Faster Payments scheme sees payment volumes having grown 9% between 2024-2025), and under FCA PS25/12’s rules for protecting consumers at payment firms’ (in effect May 2026), e-money and payment service providers (PSPs) are required to conduct daily checks for safeguarded funds, monthly reporting and annual audits. More than ever, institutions need reliable risk controls and reconciliation cycles that mirror the transactional activities of their products; i.e. instant payment rails will need to provide more frequent validation to regulators.

As a more positive implication, immediate transactional monitoring enables SAR filings to be submitted on time for enhanced investigations into justified high-risk alerts, while legitimate assets can find their way to customers instantly. This signals transparency, and a payment firms’ AML integrity, ensuring clients do not lose confidence in the protection of their hard-earned monies.

Ways to build transaction integrity with RegTech

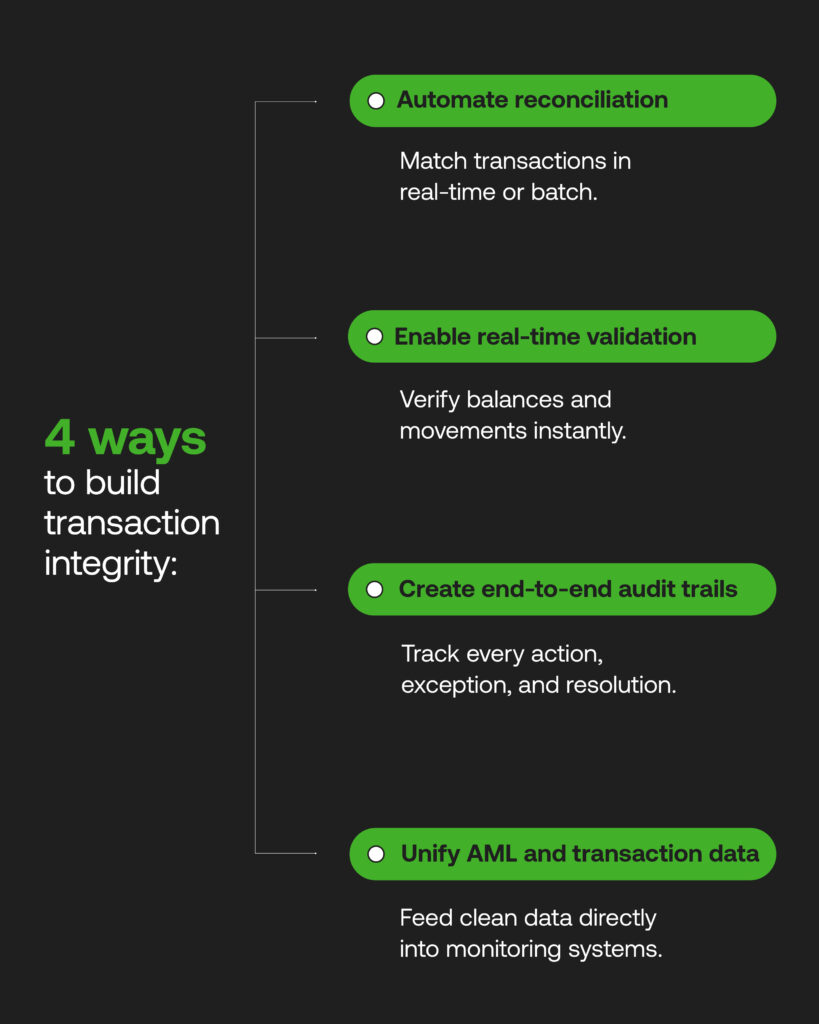

With safeguarding as valuable as installing AML transaction monitoring in the first place, the market players looking to increase the end-to-end traceability of their data will choose to integrate with RegTech platforms. Such strategic partnerships provide automations for holding and aggregating client funds, ensuring that reconciliation efforts (and their near-constant reporting to authorities) are an operational advantage, as follows:

- Advanced reconciliations: depending on a business’ fund flows, the frequency of automated reconciliation can be toggled between instant settlements, or batch payments. An integrated system will allow reconciliation to capture granular and contextual transactional data.

- In-depth safeguarding insights: transaction integrity means businesses should be able to validate an entities’ balances in real-time, and segregate them for convenient and fast reconciliation when needed.

- End-to-end audits: regulatory supervisors requiring proof of client holdings must receive reports that track all reconciliations, exceptions and resolutions. These can be automatically generated as-and-when they occur in next-gen RegTech setups.

- AML system ingestion: transaction data can be reconciled into monitoring engines within a complete compliance workflow, and ensure that SARs can be auto-filled using transparent, clean data.

These risk controls are markers for a clear evolution beyond manual and reactive monitoring. Round-the-clock capabilities increase the transaction integrity that boosts an e-payment firm or PSPs trustworthiness for consumers – who will prioritise such robust AML compliance in the clustered, competitive market for innovative financial products.

The operational evolution of AML tools

Although data analytics has been at the forefront of payment firms’ minds, the quantitative alerts of AML transaction monitoring are not all that’s needed to demonstrate transaction integrity. Now, FCA expectations call for an operational change toward real-time reporting for client fund reconciliations and safeguarding, beyond SAR requirements that are pertinent for flagging incidents of financial crime.

RegTech allows firms to unify any sporadic data systems utilised for AML processes, drawing together sensitive customer data and granting complete confidence in controlling transactional movements. When financial risk is nullified, PSPs, banks and fintechs can continue to fulfil their compliance duties – and ultimately protect the assets of the consumers at a time when voluminous instant transactions and settlements threaten any institutions not ready to face the shifting face of global payments.