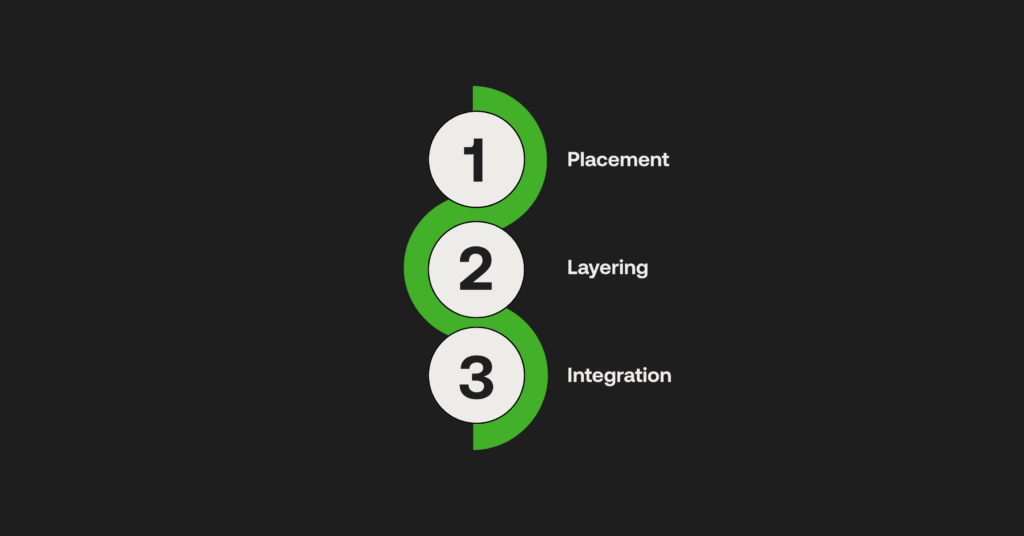

The 3 stages in money laundering explained: Placement, layering and integration

Money laundering isn’t just a compliance checkbox – it’s a lifecycle problem. Criminals don’t just transfer illicit funds once; they deliberately move them through a sequence of stages, each designed to evade regulatory controls and conceal the origin of the proceeds. Understanding the 3 stages in money laundering, namely, placement, layering, and integration, is foundational to any robust anti-money laundering (AML) programme.

The scale of money laundering is significant. Estimates from the United Nations Office on Drugs and Crime suggest it accounts for between 2% and 5% of global GDP, highlighting the scale and impact of financial crime worldwide. In the UK, the scale is also substantial, with government estimates indicating that up to £100 billion may be laundered through or within the UK each year.

In response to this scale, modern regulatory expectations increasingly emphasise lifecycle visibility across placement, layering and integration. Financial institutions are expected to demonstrate how risks evolve across the AML lifecycle, not simply identify isolated suspicious events. This reflects a broader shift toward lifecycle-aware AML approaches that recognise how financial crime risk develops over time.

The key insight many institutions overlook is that traditional rule-based monitoring struggles to identify risk that spans multiple lifecycle touch points. To meet UK regulatory expectations, firms must adopt a lifecycle-aware AML approach that connects behaviour across the full placement layering and integration journey, rather than relying solely on fragmented alerting systems.

Table of Contents

What are 3 stages in money laundering?

The three stages of money laundering are placement, layering, and integration. These stages describe how illicit funds enter the financial system, are moved and disguised through transactions, and are ultimately reintroduced into the legitimate economy.

How money is laundered in practice

As money laundering allows criminals to conceal and legitimise illegal proceeds, understanding how laundering works can help identify suspicious financial activities.

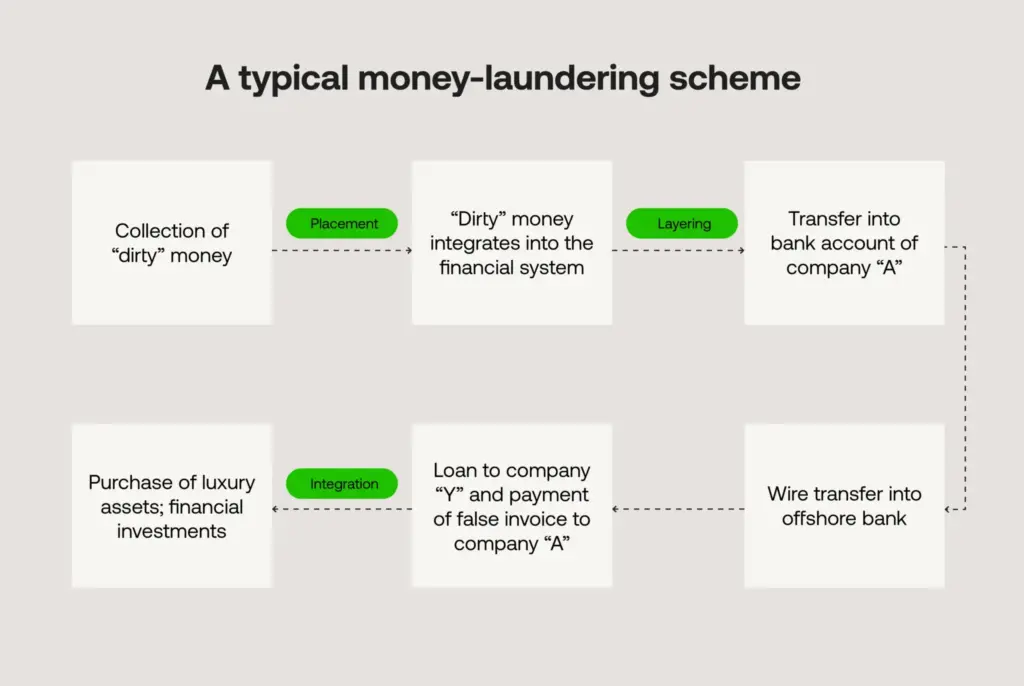

Stage 1 : Placement – introducing illicit funds into the system

The placement stage is where “dirty” money first enters the financial system. At this point, criminals try to inject illegal proceeds into legitimate channels while avoiding detection. Methods range from structuring multiple small deposits (smurfing), leveraging cash-heavy businesses, converting cash into other monetary instruments, or transferring funds through several accounts.

Placement allows launderers to discreetly bring illicit cash into banks and accounts, although unusually large or unexplained deposits can still trigger anti-money laundering alerts.

Common placement approaches in money laundering

- Making cash deposits: This remains a prime technique despite the risks. Launderers make multiple smaller deposits below reporting thresholds at various bank branches. However, banks must report unusually large or frequent cash transactions.

- Blending with legitimate income: Launderers often use cash-heavy businesses, such as laundromats or restaurants, to mix criminal proceeds with legitimate daily takings. This disguises the process of money laundering as standard business growth.

- Smurfing: Funds are split into smaller amounts and deposited across multiple accounts by different intermediaries to reduce scrutiny.

- Insider facilitation: In some cases, complicit bank employees may help launderers deposit illicit funds, ignoring regulatory reporting duties and increasing systemic risk.

- Trade-based laundering: Mis-stating the value of imports or exports – over-invoicing or under-invoicing – moves money across borders while masking its origin.

- Digital currency placement: Pseudonymous or anonymous digital currency accounts make it harder to trace funds, and the lack of centralised regulation allows transactions to bypass traditional oversight.

Traditional rule-based monitoring typically flags individual placement events based on thresholds or typologies. However, without lifecycle-aware context, early placement signals often appear low risk when viewed in isolation.

Lifecycle blind spot

A series of modest deposits over weeks may seem harmless on their own, but when viewed across the full 3 stages in money laundering, a clear risk pattern can emerge. Mapping alerts to lifecycle stages helps institutions understand how early behaviours contribute to later risk exposure.

Stage 2: Layering – disguising the origin of funds

Once the funds are inside the system, criminals enter the layering stage – a series of intricate, fast-moving transactions across accounts, jurisdictions, or financial instruments designed to distance the money from its illicit origin. This stage, often described as layering in money laundering, involves shell companies, cross-border wire transfers, or rapid asset conversions to make tracing funds increasingly difficult.

Techniques used in money laundering layering

- Multiple account transfers: Funds are moved repeatedly across accounts and institutions, both domestically and internationally, spreading them geographically to reduce the likelihood of detection.

- Shell company wire transfers: Transfers are routed through fictitious businesses, masking the true beneficial owner and making it harder to trace the origin of funds.

- Invoice manipulation: Criminals overpay invoices and receive the excess back, creating the appearance of a legitimate commercial transaction.

- Currency conversion: Money is exchanged through trades or currency exchanges to further distance it from its illicit source.

- High-value asset purchases: Funds are converted into gold, art or real estate, changing their form and making them significantly harder to trace.

- Gambling payouts: Money is gambled and cashed out as winnings, providing apparent justification for large sums that would otherwise appear suspicious.

- Cryptocurrency layering: Funds are moved between multiple cryptocurrencies to obscure tracking, with privacy coins adding a further layer of difficulty for investigators.

- Mixers and tumblers: Specialist services deliberately fragment and recombine traceable transactions to break the audit trail.

- Cross-border electronic transfers: Funds are moved between bank accounts across different jurisdictions, exploiting gaps in international oversight to conceal beneficial ownership.

Regulators increasingly expect firms to interpret layering activity as behavioural progression rather than isolated alerts. This has driven greater emphasis on analytics capable of identifying connections across fragmented data sources and product lines, making placement-layer integration analytics central to AML success when assessing the anti-money laundering stages.

Why traditional AML fails here

Rule-based monitoring may flag individual transactions, but conventional systems struggle to connect patterns across disparate data sources and customer lifecycle events. Without unified lifecycle visibility, layering activity can appear disconnected from earlier placement activity, preventing institutions from identifying risk escalations.

Stage 3: Integration – reintroducing “clean” funds

In the integration stage, illicit funds re-enter the legitimate economy – often through real estate purchases, corporate investments, or other high-value transactions that appear reputable. Here, the funds are effectively “clean,” and criminals can spend or reinvest without triggering conspicuous alarms. This stage, referred to as integration in money laundering, allows illicit proceeds to re-enter circulation with reduced suspicion.

This stage represents the most critical blind spot in traditional AML compliance because by the time funds reach this phase, they can be undetectable from legitimate sources without a comprehensive lifecycle context.

Common money laundering integration techniques

Transferring layered funds back into personal or business accounts, often to jurisdictions and entities with weak AML monitoring.

- Investment cash-outs: Laundered funds used to purchase stocks, bonds or property are cashed out, with the returns appearing as legitimate investment income.

- Luxury spending: Criminals spend laundered money openly on high-value goods such as yachts, luxury items and property, integrating funds into the legitimate economy through visible consumption.

- Shell company financing: Loans, mortgages or business investments are structured through shell companies that received layered funds, giving illicit proceeds the appearance of legitimate commercial activity.

- Cryptocurrency conversion: Digital assets accumulated during the layering stage are converted into fiat currency through exchanges, completing the transition back into the mainstream financial system.

The AML integration stage often represents the most significant visibility challenge for firms relying on fragmented systems. Without connected lifecycle intelligence, integration activity may appear legitimate because earlier risk indicators were never linked across systems or products, a common issue when organisations fail to connect the 3 stages in money laundering.

Connecting integration to the wider lifecycle

Lifecycle-aware AML connects behaviours across placement layering and integration stages, enabling institutions to detect patterns that would otherwise remain hidden. This approach aligns closely with how regulators expect firms to monitor the three stages of AML as a connected risk journey rather than isolated events.

From fragmented monitoring to lifecycle-aware AML

Understanding how money is laundered is critical. Regulatory expectations continue to evolve toward lifecycle-aware AML frameworks that provide visibility across the entire customer relationship. Supervisory guidance increasingly emphasises the importance of understanding how risk develops across placement, layering, and integration, rather than assessing activity at single points in time.

The reality is, they want AML processes and programmes that understand a customer’s behaviour through the entire process of money laundering – from onboarding through long-term relationship management.

- Lifecycle alert mapping: Alerts are linked to specific lifecycle stages, allowing compliance teams to identify how risk evolves across placement, layering and integration rather than treating each flag in isolation.

- KYC/CDD and transaction connectivity: Customer due diligence data is connected with transactional behaviour to strengthen context at each lifecycle stage, producing a more complete picture of customer risk.

- Eliminating monitoring blind spots: Siloed monitoring systems are replaced with unified oversight, closing the gaps that allow risk signals to go undetected when they cross product lines or business units.

- Lifecycle-aligned investigation workflows: Investigation processes are structured to follow AML lifecycle progression, ensuring that case-building reflects how financial crime actually develops rather than how alerts happen to fire.

- End-to-end traceability: A clear evidential thread is maintained between early placement indicators and later integration outcomes, allowing firms to demonstrate to regulators that risk was identified and tracked across the full lifecycle.

This shift reflects the growing expectation that firms demonstrate oversight of the full placement layering and integration journey, sometimes described as layering placement integration visibility within supervisory guidance.

How RelyComply is driving the move to lifecycle-aware AML

At RelyComply, we believe compliance must reflect how financial crime actually occurs – across connected behaviours rather than isolated alerts.

RelyComply delivers lifecycle-aware AML, not rule-based monitoring. Our platform connects data across onboarding, transactions, and ongoing customer activity to provide visibility across the full placement layering and integration journey.

By aligning monitoring capabilities to lifecycle progression, RelyComply enables institutions to understand how risk evolves across placement, layering, and the AML integration stage – rather than relying on disconnected rules or siloed alerts.

A single platform across placement → layering → integration allows compliance teams to identify behavioural patterns earlier, strengthen investigative context, and demonstrate alignment with evolving regulatory expectations for lifecycle-aware AML frameworks.

Through unified data coverage across products, geographies, and customer touchpoints, RelyComply enables insights that reduce the blind spots created by fragmented monitoring approaches.

Instead of disjointed alerts and disconnected workflows, compliance teams gain unified oversight and meaningful context across the full financial crime risk lifecycle.

As supervisory expectations increasingly emphasise lifecycle transparency across placement layering and integration, firms require AML technology capable of connecting risk signals across time, products, and customer behaviour. Fragmented monitoring can no longer deliver the depth of insight regulators expect.

Seeing the full lifecycle of financial crime risk

Understanding the 3 stages in money laundering – placement, layering, and integration – is not simply theoretical. It is central to designing AML programmes capable of identifying evolving financial crime risk. For organisations still asking what are 3 stages in money laundering, the answer lies in understanding how these stages connect across the full financial crime lifecycle.

Lifecycle-aware AML enables institutions to move beyond isolated rule triggers toward integrated insight across placement layering and integration behaviours.

With RelyComply’s lifecycle-aware AML platform, firms gain visibility across the entire placement → layering → AML integration stage journey, helping close blind spots and align to modern regulatory expectations that prioritise connected risk understanding over rule-based monitoring alone, reinforcing the importance of the 3 stages in money laundering.

Disclaimer: This content is provided for general informational purposes only and does not constitute legal or regulatory advice. RelyComply accepts no responsibility for the information contained herein and disclaims any liability for actions taken based on it.