Building trust and technology to beat ID theft

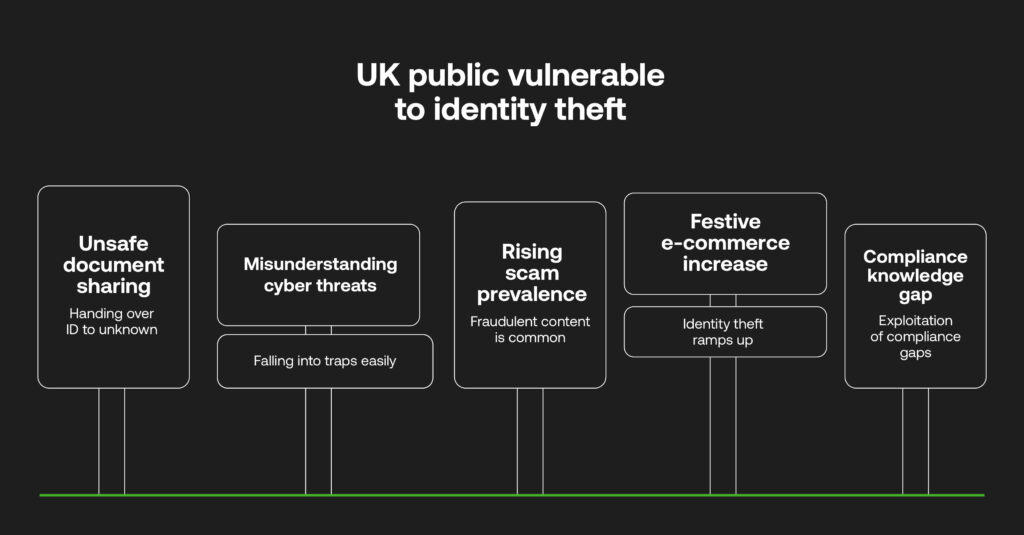

If you share a digital scan of your passport or driving license without being certain who will receive it – or why – it’s very likely to end up in the wrong hands. Alarmingly, around a third of people in the UK have already experienced some form of identity theft.

There are multiple safeguards out there, but misunderstandings around common threats in a world of rising cybercrime sees the general public falling into traps. Scams are so common that nine in ten adults have come across suspicious fraudulent content; that marks a high chance that the criminals will win, armed with people’s identities to imitate their credentials, hack into accounts elsewhere and drain their hard-earned savings.

Identity theft, noted by Experian, ramps up in the festive period when e-commerce activity hits the roof: now is the time to understand where national frameworks and institutional awareness must improve, before the gulf between public knowledge and complex anti-money laundering (AML) protocols leaves too many compliance gaps for exploitation.

Is there any protection against ID theft?

The hard numbers provide tough yet realistic reading. Identity fraud costs the UK almost £2 billion a year, making it a large contributor to the trillion-dollar industry around the world, and cases are mounting up. Large hacks affect household names and the customers that do business with them; 2025 saw retail giants Marks & Spencer and Co-op affected by online system failures, data breaches, and supply chain disruption, making public news and causing real-world effects of cybercrime.

These costs are all drained from individuals and businesses, overturning peoples’ way of life, and causing emotional stress and turmoil alongside financial calamity – particularly when data protection is becoming such a prevalent concern, and more is expected from banks and tech providers we use everyday to protect the identification we consent to give them. Phishing attacks are still the highest cases, having been experienced by up to 86% of businesses in the past twelve months alone, and still missed by many SMEs.

In order to boost nationwide safety, laws, initiatives, and coalitions are active. The 2025 Data (Use and Access) Act looks to reform digital verification services and Smart Data for finance, as well as clarify important changes to data privacy legislation. More holistically, communications regulator Ofcom looked to mitigate harm through the Online Safety Bill, passed by Parliament in 2023: holding companies to account to prevent fraudulent material (and other heinous content) proliferating in their systems that put the public at risk, and to assist compliance frameworks.

Understanding the multi-front ID threats

Ofcom, Cifas, Norton, Get Safe Online and more partners are part of this drive for education, but it needs to go far further. Most people will know to frequently choose complex passwords, store them securely and change them regularly. However, the very systems that should protect them – governmental services or databases, banks, or other financial institutions – may not be equipped with adept protections.

Ultimately, each adopts inconsistent approaches for identity verification (IDV), whether through multi-factor authentication, biometric checks or otherwise. No matter which way, these operate in their own siloes, where customer data becomes fragmented, and outdated frameworks and systems provide multiple avenues for fraudsters to act for financial gain. No matter how tight-knit someone is with their own logins, they may still be left vulnerable by services that must adhere to data-centric legislation.

As a way to strengthen UK citizens’ access to government services, and to clamp down on illegal working and create intelligent business data, a proposed Digital ID ‘Brit Card’ is in the works. It has, however, been met with public unease citing exclusion and opaque data intentions. Networks that operate with consumer data (no matter the well-intentioned thought behind its use) have to be transparent to improve the trustworthiness of advanced IDV – especially for anti-fincrime controls.

ID theft alert! A business guide to fighting back

A business-to-consumer relationship is all built on trust, no less for data privacy. Awareness is a shared responsibility between both, working together to identify suspicious signs, detect and report wrongdoing.

And when obligated to protect personal information and define its fair and lawful use under regulations set by the Information Commissioner’s Office (ICO), organisations must implement the use of exemplary AML frameworks to ensure fraud prevention and avoid the harmful knock-on effects of breaches:

- Adopt robust risk assessment controls: a risk-based AML approach triggers alerts for anomalous activity from high-risk individuals, beneficial owners or regions.

- Adopt continuous verification: following onboarding, AI-driven know your customer (KYC) controls continually update risk profiles with correct information for future-proofed compliance.

- Unify systems: sporadic outdated datasets are prone to hackers, where one-view systems are encrypted, secure and speed up the detection and reporting of suspicious activity to authorities.

- Leverage customer data intelligently: behavioural biometrics and device recognition can detect any account takeover risks, while AI-driven real-time IDV can scan identity documents against governmental records and accurately identify the nuances of synthetic identities.

- Partner with RegTech: ongoing AML expertise and cloud-based integrations help businesses stay flexible to data privacy compliance changes and cyber threats.

- Collaborate across borders: ID theft does not respect geography, where collaborative forums and partnerships increase IDV knowledge and capability, as well as foster a transparent AML culture.

The power of consumers in ID protection

Plus, in the UK and otherwise, there needs to be better digital education as more citizens utilise phones and laptops to get online, to then access sensitive portals for healthcare and taxes, to apply for credit, or to gain a loan.

There’s plenty of resources available, where companies should run repeated training and create educational content to keep their customers in-the-loop around cybersecurity and their responsibilities to prevent their data being compromised:

- Staying vigilant: security advice through the UK’s Met Police and Cyber Aware websites should be highlighted, to promote cautiousness on ID sharing via digital channels, keeping devices and online accounts secure.

- Increasing reporting: many consumers feel embarrassed for having data compromised, or from experiencing a ‘near miss’ from a financial scam or by finding a potentially suspicious website – investigations made to financial institutions, Action Fraud or the National Cyber Security Centre (NCSC) will improve intelligence to cut out criminal activity.

- Understanding data rights: the ICO can help education around consumer rights for data protection, where subjects can control their data or seek recourse for misuse.

- Holding regulated institutions to account: Subject Access Requests can be exercised to learn how data is verified and used by any businesses.

With greater knowledge comes open cybercrime dialogue across the board; a trust-building exercise put into effective investigation and prosecution through dynamic digital AML solutions at governments, regulators, financial institutions and more.

The tech-based next steps

Learn more in our latest white paper – Closing the Gaps in Financial Crime Prevention – where we see how layered IDV, continuous monitoring, and collaborative partnerships all play such a pivotal role in building resilience on the frontline against identity thieves.