Why collaboration can help fight money laundering

Table of Contents

Have you heard the story of Franklin D. Roosevelt murdering his grandmother?

There should be an emphasis on ‘story’, as this urban myth is based on a dark joke FDR allegedly played at important receptions. Politely whispering to his esteemed guests that he’d killed his grandmother was a way to work out who was listening properly. Reported responses included “Keep up the good work” and, from one Wall Street Banker, “She certainly had it coming.”

What relevance does this have to financial crime?

As it would seem, quite a lot. Illegal behaviour, even when carried out in plain sight, often slips under the radar. Whether nefarious activity pertains to money laundering, racketeering, or trafficking, it’s up to a combined network of lawmakers, regulators, and financial services firms to adopt stringent anti-money laundering (AML) processes and technologies to clamp down on the facilitated crime that affects everyday lives on a devastating scale.

The need for collective success

Such money laundering activity is not relegated to gripping thriller plots but is a real chapter in recent history.

I recently read the book ‘The Snakehead, documenting the vast human smuggling operation built by Sister Ping in New York. At her empire’s magnitude, a ship of undocumented Chinese immigrants met a tragic end in the Golden Venture disaster 1993, signalling our collective failure to save innocent lives.

Despite being on the authorities’ radar, Sister Ping eluded capture. Why? Mostly due to inefficiencies and inadequate tools, and, as one quote in the book attests, “Any international effort to regulate international crime will only be as good as the least efficient nation involved.” It certainly resonates. These efficiencies still exist, and we must rise above them to better fight against financial criminals and their extensive networks.

History and Future Hope

If Sister Ping’s story represents the loopholes of the past, the digitalization of banking and monetary transactions has provided new avenues for sophisticated fraudulent methods and highlighted the complex feats criminals will go to to exploit financial systems.

The threat we face is colossal. It’s estimated that the amount of money laundered globally in one year is 2% to 5% of global GDP—that’s between $800 billion and $2 trillion in current US dollars. This isn’t just a dent; it’s a gaping hole that can discourage foreign investment and lead to economic collapse. Between 2008 and 2018, global banks were penalised over $26 billion for AML, know your customer (KYC), and sanctions violations. These hefty fines reflect the steep price institutions pay for continual lapses in their AML strategies.

Adaptation is more vital than ever. We face ever-evolving financial transformations through the likes of blockchain and cryptocurrencies, which dwarf more simplistic wire transfers. However, another tech phenomenon, artificial intelligence, can also provide new applications to benefit AML practices.

The case for AI

AI revolutionises manual risk-mitigation methods by using automation techniques to amplify the workload of human hands. It can scan decades’ worth of transactions to spot anomalies in minutes rather than months or even years. AI also provides ample potential for advanced data analysis. But it must be taken with a pinch of salt. If not curated carefully, AI algorithms might become sources of bias and misinformation. A staggering 95% of system-generated alerts reported as ‘false positives’ show the scale of the challenge.

Despite the pitfalls, AI is not the sci-fi scaremonger it is often billed as. While carrying risks in the wrong hands, the critical synergy between humans and technology is needed to improve AML processes. AI provides insights, but humans lend context. Likewise, there are multiple practical AI uses in financial crime compliance from high-profile organisations:

Standard Chartered has invested in a system to automate parts of the risk-compliance process, including AML. Machine learning reviews transactions, which has reportedly resulted in a 40% time reduction in certain compliance processes.

BBVA, a Spanish bank at the forefront of banking innovation, has been leveraging big data and AI to spot anomalies (even those that deviate slightly from established norms). Its detection rate of suspicious activities has increased by 200%, with the aim of improving financial crime prevention.

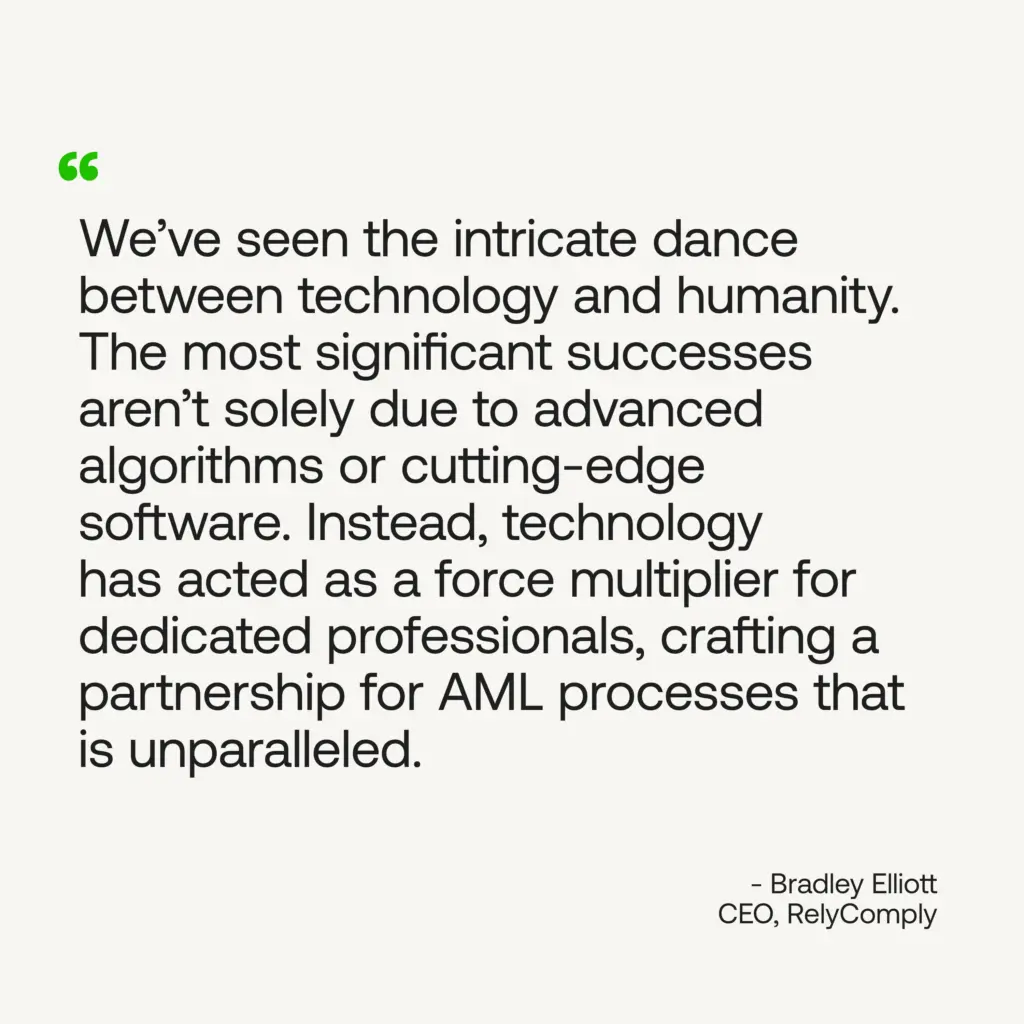

We’ve seen the intricate dance between technology and humanity through our partnerships with our customers. The most significant successes aren’t solely due to advanced algorithms or cutting-edge software. Instead, technology has acted as a force multiplier for dedicated professionals, crafting an unparalleled partnership for AML processes.

From dream to reality

Staring into the horizon, we also envision a combined financial ecosystem robust against threats and exploitation, but it involves active participation. It takes more than embracing evolving technologies and integrations, including reforming policies, fostering collaborations, and maintaining an ethos of continuous learning and vigilance.

Disclaimer

This article is intended for educational purposes and reflects information correct at the time of publishing, which is subject to change and cannot guarantee accurate, timely or reliable information for use in future cases.