PEP screening best practices: a guide for compliance teams

A politically exposed persons check (PEP check) is one of the most consequential steps in any AML compliance programme. Get it right, and you’re identifying elevated risk before it becomes your problem. Get it wrong – or worse, treat it as a one-time box to tick – and you’re exposed to regulatory censure, reputational damage, and the real possibility of facilitating corruption or money laundering.

The stakes are well understood. What’s less clear, for many institutions, is where their current approach falls short.

Table of Contents

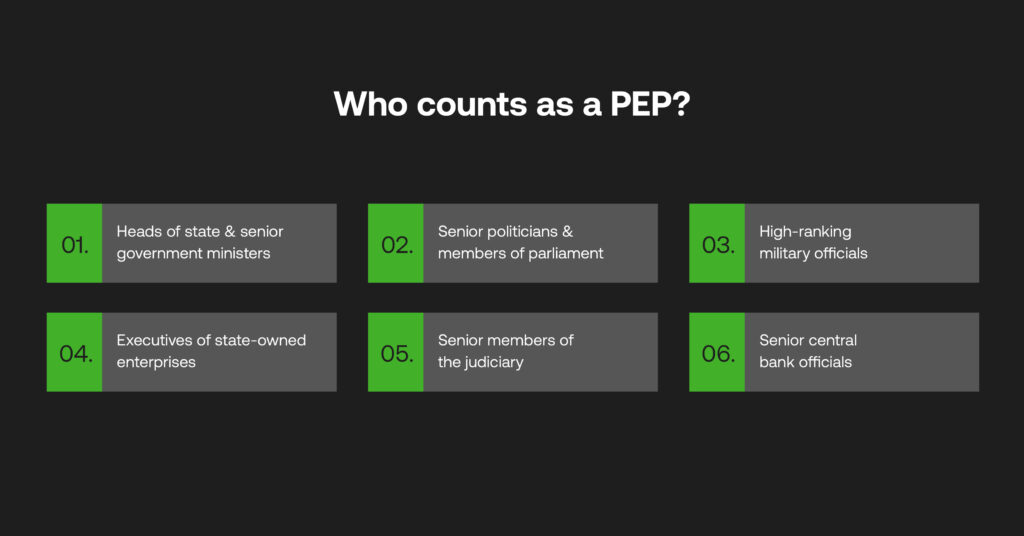

What does PEP stand for?

PEP stands for Politically Exposed Person. In banking and financial services, a PEP is an individual who holds – or has held – a prominent public function that gives them influence over public resources or policy decisions.

Common PEP examples include:

- Heads of state and senior government ministers

- Senior politicians and members of parliament

- High-ranking military officials

- Executives of state-owned enterprises

- Senior members of the judiciary

- Senior central bank officials

Crucially, the PEP definition extends to immediate family members and known close associates – individuals who carry elevated risk by proximity, even without a formal role themselves. This is a critical distinction that many institutions overlook.

What is PEP in AML and KYC?

In AML (anti-money laundering) and KYC (know your customer) frameworks, PEP screening is a mandatory risk management process. The rationale is straightforward: individuals with access to public funds or policy influence present a higher risk of involvement in bribery, corruption, and money laundering. Financial institutions are required under FATF recommendations, the EU’s 4th and 5th Anti-Money Laundering Directives (4AMLD/5AMLD), and national regulatory regimes to identify PEP customers and apply Enhanced Due Diligence (EDD) accordingly.

PEP meaning in KYC, then, goes beyond a simple status flag. It triggers a distinct set of obligations — from source of wealth verification to senior management sign-off — that apply throughout the customer lifecycle, not just at onboarding.

What makes a PEP check effective?

Effective PEP screening rests on three pillars.

1. Data quality: The foundation of reliable PEP screening

Your screening is only as good as the lists you’re checking against. A reputable, regularly-updated global PEP list is non-negotiable. Proprietary or outdated sources introduce blind spots — particularly across jurisdictions where public records are fragmented or unreliable.

When evaluating a PEP list or database provider, look for: global coverage, update frequency, inclusion of associates and family members, and multi-language/transliteration support.

2. Risk-based categorisation

Not all PEPs carry the same risk. A former local councillor and a serving foreign head of state require very different levels of scrutiny. FATF guidance and 4AMLD/5AMLD both emphasise a risk-based approach — calibrating your EDD to the nature and degree of the individual’s exposure, their country risk profile, and the source of their wealth.

In PEP finance terms, this means tiering your PEP customers by risk level and applying proportionate controls rather than a single blanket treatment.

3. Ongoing monitoring, not point-in-time screening

A customer who is not a PEP today may become one tomorrow. Someone who left office a year ago may still present elevated risk — FATF guidance recommends a minimum 12-month cool-down period after leaving public office, with many compliance frameworks extending that window further depending on the seniority of the role.

PEP screening must be continuous: triggered by status changes, adverse media alerts, and scheduled re-reviews — not just at onboarding.

Where most institutions go wrong with PEP screening

Siloed data: KYC records, transaction data, and adverse media alerts exist in separate systems. A PEP match that should trigger an EDD review gets missed because no one is joining the dots. Integrated compliance platforms eliminate this fragmentation.

Inconsistent thresholds: Without a documented, risk-based framework, different analysts reach different conclusions on the same PEP customer profile. This inconsistency creates regulatory exposure and internal audit risk.

Manual processes at scale: Screening a PEP isn’t just about matching a name — it’s about managing false positives intelligently so your compliance team can focus on genuine risk. Automated name-matching with fuzzy logic, transliteration handling for non-Latin scripts, and AI-assisted alert triage dramatically reduce noise without sacrificing accuracy.

Failure to screen close associates: Beneficial ownership structures, shell companies, and nominee arrangements are routinely used to distance PEPs from financial activity. A robust KYB (Know Your Business) process that maps ownership and control — not just the named individual — is essential to closing this gap.

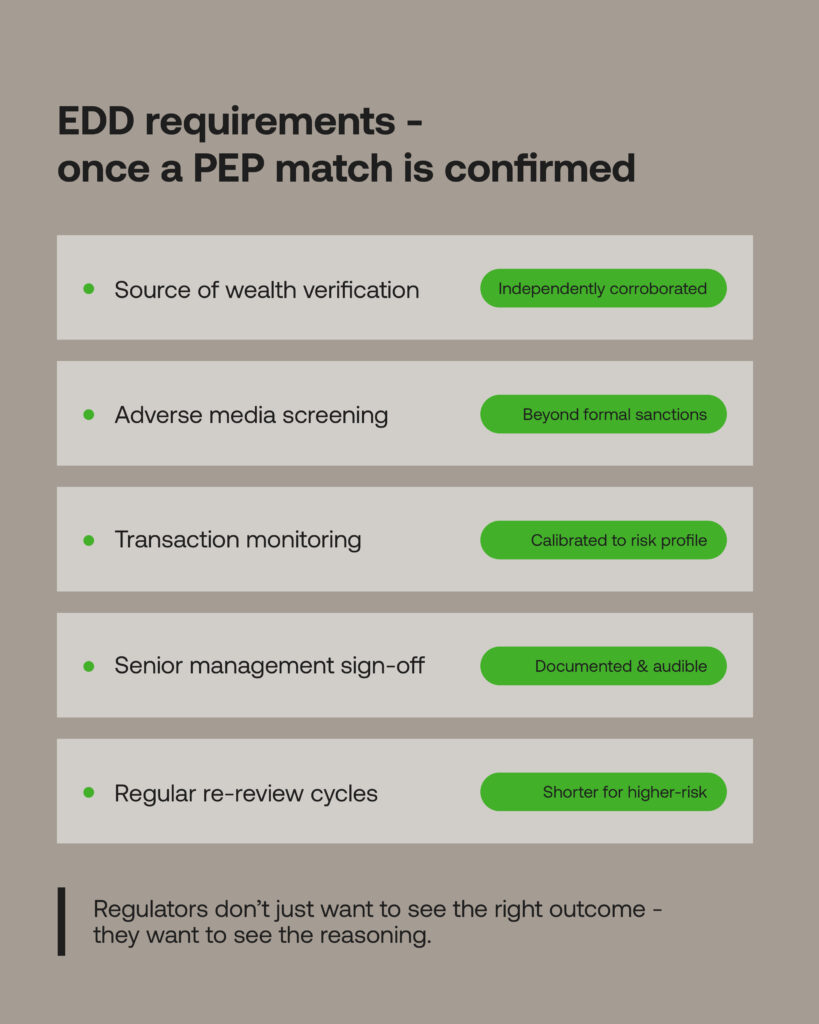

Enhanced Due Diligence for PEP customers

Once a PEP match is confirmed, EDD isn’t optional. For any PEP customer, your Enhanced Due Diligence process should include:

- Source of wealth and source of funds verification — independently corroborated where possible, not simply self-declared

- Adverse media screening — structured checks across credible news sources, watchlists, and law enforcement databases, flagging negative coverage beyond formal sanctions

- Transaction monitoring calibrated to the risk profile — unusual patterns, high-value transfers to high-risk jurisdictions, and behaviour inconsistent with the stated purpose of the account

- Senior management sign-off — for higher-risk PEP relationships, approval should sit at an appropriate level of seniority, documented and auditable

- Regular re-review cycles — with shorter intervals for higher-risk profiles

Documentation throughout is critical. Regulators don’t just want to see the right outcome — they want to see the reasoning.

The technology imperative for PEP screening

PEP screening at any meaningful scale requires automation. The sheer volume of data involved — multiple PEP lists, continuous updates, complex beneficial ownership structures, cross-border activity — is beyond what manual processes can reliably manage.

The best compliance platforms do more than match names against a PEP list. They:

- Aggregate and reconcile PEP data from multiple sources

- Apply risk-weighted scoring to prioritise genuine alerts

- Surface adverse media in context, not just raw flags

- Generate audit trails that hold up under regulatory scrutiny

- Reduce false positive burden to combat alert fatigue — one of the most damaging and least-discussed problems in financial crime compliance

Critically, the system has to be configurable. Risk appetite varies by institution, by jurisdiction, by product type. A rigid, one-size-fits-all approach to PEP screening will either over-flag and paralyse operations, or under-flag and create exposure.

The standard compliance teams need to meet

PEP checks are not a formality. They’re one of the most direct mechanisms financial institutions have for preventing corrupt funds from entering the financial system – and for protecting themselves from the consequences of failing to do so.

Best practice means robust data, a documented risk-based framework, automated screening with intelligent alert management, continuous monitoring, and EDD that is genuinely enhanced – not merely procedural.

If your current PEP screening process was designed around onboarding and hasn’t evolved since, it’s time to revisit it.

Screen smarter. Act faster.